Corporate renewable energy India has crossed a turning point in 2026. Five years ago, sustainability teams drove this conversation armed with ESG targets, brand narratives, and voluntary commitments. Today, CFOs drive it armed with electricity bills, BRSR filing deadlines, and supply chain exclusion letters from European buyers. The conversation changed because the stakes changed.

India’s commercial and industrial sector accounts for 40 to 45 percent of total national electricity demand. For most of that sector, electricity is not a minor overhead it is a top-three operating cost. Furthermore, grid tariffs for industrial consumers have risen 4 to 7 percent annually for the past decade, while solar power purchase agreement rates have stayed flat or declined. Consequently, the financial case for clean energy now argues itself in a board meeting without a sustainability narrative attached.

However, cost is only one of five forces reshaping how corporate India thinks about renewable energy. This guide explains all five, shows what the shift looks like in practice, and outlines the specific steps forward-thinking businesses take in 2026.

| 274 GW

India’s installed renewable capacity March 2026 |

40–45%

Share of C&I in India’s total electricity demand |

4–7%

Annual grid tariff escalation for industry |

Rs 3.40

Typical group captive solar landed cost per unit |

From CSR Optics to CFO Agenda How Corporate Renewable Energy India Changed

Until 2021, most large Indian corporates treated renewable energy as a sustainability department initiative. The typical outcome was a rooftop solar installation on the headquarters building, a press release, and a line in the annual report. Meanwhile, the factory floor which consumed 90 percent of actual electricity remained entirely on the DISCOM grid.

Three things changed that dynamic. First, electricity bills crossed a threshold where CFOs could no longer rationalise grid dependence. For a mid-sized textile mill in Maharashtra paying Rs 12 per unit in 2026, energy now represents 25 to 35 percent of total production cost. Second, SEBI mandated Scope 2 disclosure in the BRSR framework. Therefore, renewable energy procurement became a measurable compliance requirement, not an optional statement. Third, international buyers started rejecting suppliers who could not document their carbon footprint.

As a result, corporate renewable energy India has shifted from a single team’s agenda to a board-level risk management decision. Furthermore, the speed of this shift accelerated through 2024 and 2025 as open access solar infrastructure matured, group captive structures simplified procurement for MSMEs, and module costs fell to levels that made even cautious finance directors pay attention.

The Numbers That Forced Corporate India to Pay Attention

Grid Tariffs Rose Faster Than Any Other Input Cost

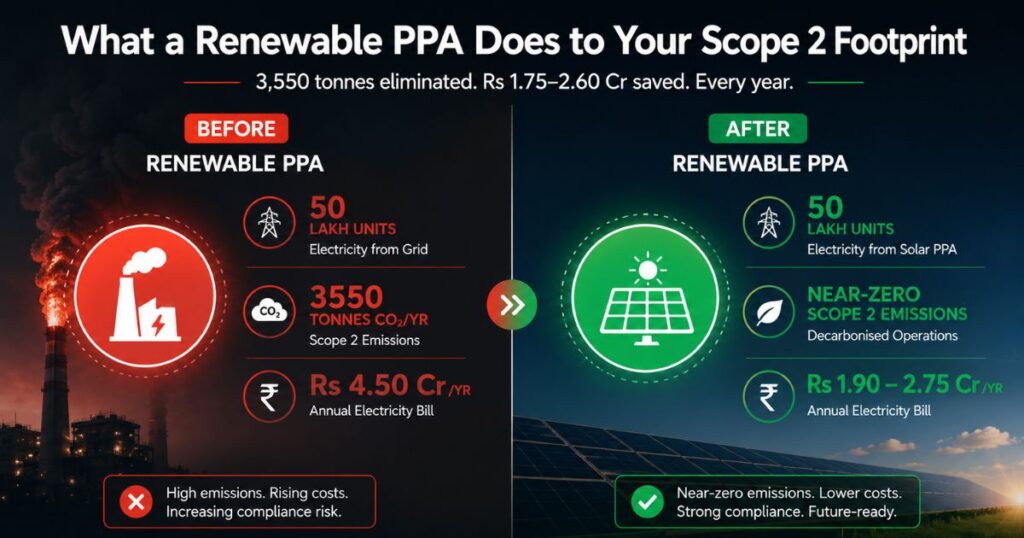

India’s industrial electricity tariffs have climbed every year without exception for the past decade. In Maharashtra, large HT industrial consumers now pay Rs 7.48 to Rs 12 per unit in FY2026 depending on load factor, voltage level, and time-of-day schedule. Moreover, these tariffs do not include fuel and power purchase adjustment charges, which DISCOMs levy on top of base rates to recover procurement cost overruns.

Solar energy, in contrast, costs Rs 2.20 to Rs 2.80 per unit at the PPA rate and Rs 3.40 to Rs 5.50 per unit all-in after wheeling, CSS, and banking charges. Therefore, the arbitrage between grid power and clean solar power has never been wider. Additionally, solar costs do not escalate with fuel prices or regulatory revisions. A 25-year PPA rate locked today stays locked regardless of what happens to coal prices or DISCOM finances between now and 2051.

India’s Grid Carries 0.71 kg CO2 Per kWh and Global Buyers Are Watching

India’s national grid emission factor stands at 0.71 kg CO2 per kWh, as published by the Central Electricity Authority. A factory consuming 1 lakh units per month therefore generates 71 tonnes of Scope 2 CO2 every single month 852 tonnes per year. Furthermore, this figure does not stay abstract for long. European buyers under the EU CSRD now require suppliers to report and reduce Scope 2 emissions from their Indian manufacturing operations. Consequently, an Indian exporter who cannot demonstrate a renewable energy procurement strategy faces a real risk of supply chain exclusion not a theoretical one.

Five Reasons Corporate India Is Rethinking Renewable Energy Right Now

Corporate renewable energy India is not driven by a single force. Instead, five separate pressures converge in 2026 to create a decision environment where staying on the DISCOM grid requires more justification than moving to clean energy. Here are all five.

-

SEBI BRSR Compliance

India’s top 1,000 listed companies by market capitalisation must now disclose Scope 1 and Scope 2 greenhouse gas emissions under SEBI’s Business Responsibility and Sustainability Reporting framework. The BRSR Core a subset of assured disclosures requires companies to report the percentage of energy consumed from renewable sources. Additionally, institutional investors and ESG rating agencies use BRSR data to assess climate risk. Therefore, a company with undocumented and unreduced Scope 2 emissions now faces downward ESG rating pressure. SEBI’s BRSR framework documentation details the exact Scope 2 reporting requirements.

-

EU CBAM and CSRD International Trade at Stake

The European Union’s Carbon Border Adjustment Mechanism taxes imports from carbon-intensive supply chains. Furthermore, the EU Corporate Sustainability Due Diligence Directive requires MNCs to assess and report the ESG performance of their Indian suppliers. As a result, Indian exporters in textiles, pharma, auto components, and specialty chemicals now receive carbon questionnaires from their EU buyers as a standard part of vendor qualification not as an optional ESG inquiry.

-

Grid Tariff Lock-In Solar Fixes Your Energy Cost at Rs 3.40 for 25 Years

A group captive solar PPA locks your all-in electricity cost at Rs 3.40 to Rs 4.00 per unit for the full PPA tenure. Meanwhile, DISCOM tariffs rise 4 to 7 percent annually. The difference between what you pay on grid in 2026 and what you would pay in 2041 is not linear it compounds. Consequently, a company that delays a renewable energy procurement decision by five years misses a cumulative cost advantage that never returns.

-

Open Access Now Works at the 100 kW Scale

The Green Energy Open Access Rules 2022 reduced the minimum open access threshold from 1 MW to 100 kW. Furthermore, the GOAR portal centralised SLDC approvals and introduced a 15-day deemed approval provision. As a result, medium-sized factories and commercial establishments that previously did not qualify for open access now access the same economics as large industrials. Additionally, group captive structures allow MSME clusters to pool demand and share a single plant making solar accessible to even smaller individual consumers.

-

Accelerated Depreciation and GST ITC The Tax Case Is Complete

Section 32 of the Income Tax Act allows 40 percent accelerated depreciation on solar assets in Year 1 for commercial businesses, and 60 percent for manufacturing companies. Furthermore, GST Input Tax Credit recovery on system components typically returns 5 to 12 percent of total system cost in Year 1. Therefore, for profitable businesses with taxable income, the combination of cost savings, tax shield, and carbon documentation makes a captive or group captive solar investment one of the highest-IRR capital allocations available in India today.

For the full financial case with 25-year modelling, read our guide: Solar Payback Period for C&I India 2026. For the Section 32 accelerated depreciation rules, refer to the Income Tax Act documentation at incometaxindia.gov.in.

What Corporate Renewable Energy Looks Like in Practice in India

The shift in corporate renewable energy India is not hypothetical. Large corporates, mid-sized manufacturers, and MSME clusters across India are already executing renewable energy procurement at scale. Furthermore, the diversity of project types from rooftop captive PPAs to group captive ground-mount structures to virtual PPAs for multi-location MNCs reflects a market that has matured past the pilot stage.

Companies That Have Already Made the Move in Corporate Renewable Energy

Unilever executed a 45 MW solar PPA in Rajasthan to supply 10 of its collaborative manufacturing partners explicitly targeting Scope 3 emission reductions across its supply chain. Moreover, Microsoft signed a 437.6 MW green attribute contract with ReNew Power, including a community investment fund aligned with its 2030 carbon-negative commitment. These are not token gestures they represent multi-decade contracted procurement strategies built around verified renewable generation data.

In India’s MSME sector, the growth of group captive structures is equally significant. Textile clusters in Surat and Indore, auto component manufacturers in Pune, and food processing estates in Madhya Pradesh are forming special purpose vehicles to access group captive economics CSS exemption, accelerated depreciation, and verified Scope 2 reduction at a scale no individual factory could access alone.

Additionally, data centre operators building new capacity in India now treat renewable energy procurement as a prerequisite not a preference. As a result, every major greenfield hyperscale development in India in 2026 includes a renewable PPA or captive solar structure as part of the original project design.

The Cost of Waiting What Happens to Companies That Don’t Rethink

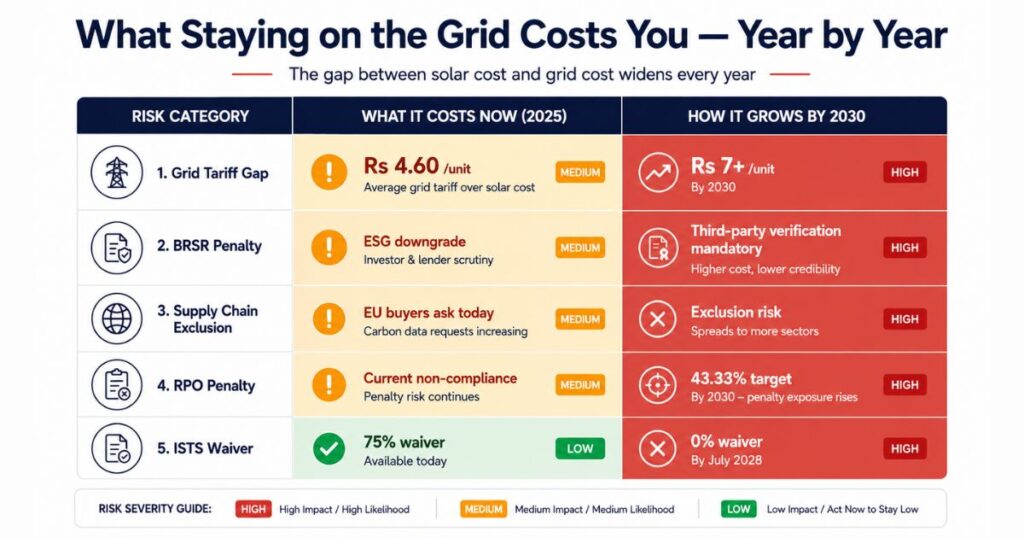

The question corporate India used to ask was: “Should we do renewable energy?” In 2026, the more accurate question is: “What is the cost of not doing it?” The answer is specific, measurable, and growing every year.

| Risk Category | What It Costs Now | How It Grows by 2030 |

| Grid Tariff Escalation | Rs 8–12/unit today vs Rs 3.40 solar | Grid reaches Rs 11–17/unit by 2030 at 5% annual rise |

| BRSR ESG Rating | Scope 2 undisclosed = downward rating | Assurance requirements tighten; third-party verification mandatory |

| Supply Chain Exclusion | EU buyers require carbon data now | CBAM extends to more sectors; exclusion broadens |

| RPO Penalty | Non-compliant consumers face penalties under Energy Conservation Act | RPO targets rise to 43.33% by 2029-30 |

| Policy Window Narrowing | ISTS waiver at 75% in FY26 | ISTS waiver reaches 0% by July 2028 inter-state costs rise permanently |

The Renewable Purchase Obligation for designated consumers reaches 43.33 percent by FY2029-30, per the Ministry of Power’s October 2023 notification. Companies that fail to meet RPO targets face penalties under the Energy Conservation Act. Furthermore, the penalty escalates with the shortfall. Consequently, the cost of inaction is not hypothetical it is a scheduled regulatory charge.

For the full explanation of how Scope 2 emissions translate to BRSR obligations, read our detailed guide: Scope 1, 2 and 3 Emissions A Complete Guide for Businesses.

How Corporate India Should Approach Renewable Energy in 2026

Corporate renewable energy India does not require a complete energy strategy overhaul to begin. Instead, it requires three specific actions in sequence each building the foundation for the next. Furthermore, each action produces a standalone output that serves compliance and financial reporting purposes even if the full procurement decision takes longer than expected.

Step 1 Establish Your Scope 2 Baseline

Pull 12 months of electricity bills. Calculate your annual consumption in kWh. Multiply by the CEA grid emission factor 0.71 kg CO2 per kWh to establish your Scope 2 baseline. Additionally, identify your contracted demand in kW or kVA and your tariff category. This baseline is the foundation of your BRSR disclosure, your SBTI target, and your PPA sizing calculation. Moreover, it takes less than a working day to produce.

For a full explanation of the GHG accounting framework, read: Scope 1, 2 and 3 Emissions A Complete Guide.

Step 2 Model the Right Procurement Structure

Run a landed cost model for your specific state and load profile across three structures: on-site captive PPA, group captive open access, and third-party PPA. Compare each against your current DISCOM tariff. Furthermore, model the CSS and Additional Surcharge for your state because the same solar PPA rate produces very different net savings depending on whether you are in Karnataka (low CSS) or Maharashtra (high CSS).

Additionally, factor in the accelerated depreciation benefit if you choose a captive or group captive structure. For a profitable manufacturing business paying 25 percent corporate tax, the Year 1 tax saving alone covers 15 to 20 percent of system cost. Consequently, effective payback for well-structured corporate renewable energy projects in India runs between 2 and 4 years.

For state-wise charge data, read: Open Access Solar Charges Explained India 2026.

For a full open access guide for your sector: Open Access Solar for MSMEs and Factories.

Step 3 Execute Before the Policy Window Narrows

Two policy parameters create urgency in 2026. First, the ISTS charge waiver for inter-state renewable projects currently stands at 75 percent for FY26 falling to 50 percent in FY27, 25 percent in FY28, and zero from July 2028. Therefore, projects commissioned in FY26 or early FY27 lock in a significantly lower inter-state cost structure than those commissioned later. Second, commissioning before October 3 of any financial year captures full accelerated depreciation the half-year rule halves the benefit for later commissionings. Consequently, the commissioning date is a financial decision, not just a construction milestone.

For the Bureau of Energy Efficiency’s energy efficiency and renewable compliance framework, refer to: bee.gov.in. For MNRE’s current renewable energy policy framework, refer to: MNRE official documentation at mnre.gov.in.

Frequently Asked Questions About Corporate Renewable Energy India

Q: Why is corporate renewable energy India growing so fast in 2026?

A: Three forces converge simultaneously. First, solar PPA rates at Rs 2.20 to Rs 2.80 per unit are significantly cheaper than industrial DISCOM tariffs of Rs 7 to Rs 12 per unit in most states. Furthermore, SEBI’s BRSR framework mandates Scope 2 disclosure for India’s top 1,000 listed companies, making renewable procurement a measurable compliance requirement. Additionally, EU buyers now require carbon data from Indian suppliers under the CSRD and CBAM frameworks. As a result, corporate renewable energy India has shifted from sustainability strategy to board-level risk management across sectors including textiles, auto components, pharma, and data centres.

Q: What is the best renewable energy option for a mid-sized Indian corporate in 2026?

A: For most mid-sized Indian corporates consuming Rs 10 to Rs 50 lakh per month in electricity a group captive open access solar PPA delivers the best combination of savings, compliance value, and capital efficiency. Group captive structures provide full CSS and Additional Surcharge exemption under the Electricity Act 2003, accelerated depreciation on the equity portion, verified REC generation for BRSR and RE100 reporting, and landed costs of Rs 3.40 to Rs 4.00 per unit all-in. Moreover, group captive removes the need for any individual company to own and operate its own plant the developer manages construction and operations.

Q: How does renewable energy help Indian corporates with BRSR compliance?

A: India’s BRSR framework requires companies to disclose Scope 2 GHG emissions the carbon footprint of purchased electricity and report the percentage of energy from renewable sources. Every unit of electricity sourced through a renewable PPA reduces your Scope 2 number by eliminating 0.71 kg CO2 per kWh from your inventory. Furthermore, the REC generated by your PPA plant provides the documented market-based evidence that BRSR assurance auditors require. Consequently, a well-structured corporate renewable energy procurement in India produces both a financial saving and a BRSR-compliant carbon reduction record from the same contract.

Q: How much can an Indian corporate save by switching to renewable energy?

A: Savings depend on your state, tariff category, and procurement model. However, for a typical industrial consumer in Madhya Pradesh paying Rs 8.80 per unit and moving to a group captive solar PPA at Rs 3.40 per unit all-in, the saving is Rs 5.40 per unit. On 2 lakh units per month, that is Rs 10.8 lakh per month Rs 1.3 crore per year. Moreover, this saving grows every year as DISCOM tariffs escalate while solar PPA rates stay fixed. Over 25 years at 4.5 percent annual tariff escalation, the total saving on the same 2 lakh units per month exceeds Rs 5 crore from a single procurement decision.

Q: What is the Renewable Purchase Obligation and how does it affect Indian corporates?

A: The Renewable Purchase Obligation (RPO) requires designated large consumers to source a defined percentage of their electricity from renewable sources. The Ministry of Power’s October 2023 notification sets the total RE target at 43.33 percent by FY2029-30. Companies that fall short face penalties under the Energy Conservation Act. Furthermore, RPO compliance tracking is separate from BRSR a company can meet RPO through REC purchases but still face BRSR scrutiny for insufficient Scope 2 reduction. Therefore, a physical renewable PPA that delivers both actual green electricity and RECs is more comprehensive than REC-only procurement strategies.

Q: How long does it take to commission a corporate renewable energy project in India?

A: A rooftop captive solar project (100 kW to 2 MW) typically takes 6 to 12 weeks from contract signing to commissioning. A ground-mounted open access or group captive project (500 kW to 10 MW) typically takes 4 to 8 months, including SLDC approval, EPC execution, and grid synchronisation. Fast states Madhya Pradesh, Karnataka, Rajasthan, Gujarat process SLDC applications in 5 to 10 weeks for complete submissions. Maharashtra and UP take 12 to 20 weeks. Commissioning before October 3 of the financial year captures full accelerated depreciation making this timeline a financial planning priority, not just a construction milestone.

Bottom Line

Corporate renewable energy India has moved past the threshold where it requires a sustainability narrative to justify. The financial case closes itself: solar at Rs 3.40 per unit versus grid at Rs 9 to Rs 12 per unit, locked for 25 years, with a Year 1 tax shield, verified carbon reduction documentation, and supply chain compliance value bundled in. Furthermore, the regulatory environment in 2026 makes delay progressively more expensive rising RPO targets, narrowing ISTS waivers, and mandatory BRSR disclosure all point in one direction.

The companies that move in FY26 capture the widest cost arbitrage, the most favourable ISTS terms, and the earliest BRSR compliance track record. Those that wait face a narrower window, higher charges, and a compliance backlog that compounds annually. Consequently, the question for corporate India in 2026 is no longer whether to rethink renewable energy. It is how quickly the rethinking produces an executed contract.

Solarsure works with C&I businesses, factories, and MSME clusters across Madhya Pradesh and Rajasthan to model the right structure, execute the right procurement, and deliver the right documentation. The starting point is a free site assessment and Scope 2 baseline available at solarsure.in.